0001743745false2019FYP3YP3YP4YP0Y00017437452020-01-012020-12-31iso4217:USD00017437452020-06-30xbrli:shares0001743745us-gaap:CommonClassAMember2021-03-260001743745us-gaap:CommonClassBMember2021-03-260001743745us-gaap:CommonClassCMember2021-03-2600017437452020-12-3100017437452019-12-31iso4217:USDxbrli:shares0001743745us-gaap:CommonClassAMember2020-12-310001743745us-gaap:CommonClassAMember2019-12-310001743745us-gaap:CommonClassBMember2020-12-310001743745us-gaap:CommonClassBMember2019-12-310001743745us-gaap:CommonClassCMember2020-12-310001743745us-gaap:CommonClassCMember2019-12-3100017437452019-01-012019-12-310001743745gnln:RedeemableClassBUnitsMember2018-12-310001743745gnln:MembersEquityMember2018-12-310001743745us-gaap:CommonClassAMember2018-12-310001743745us-gaap:CommonClassBMember2018-12-310001743745us-gaap:CommonClassCMember2018-12-310001743745us-gaap:AdditionalPaidInCapitalMember2018-12-310001743745us-gaap:RetainedEarningsMember2018-12-310001743745us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-310001743745us-gaap:NoncontrollingInterestMember2018-12-3100017437452018-12-310001743745gnln:RedeemableClassBUnitsMember2019-01-012019-04-230001743745gnln:MembersEquityMember2019-01-012019-04-2300017437452019-01-012019-04-230001743745us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-04-230001743745us-gaap:AdditionalPaidInCapitalMember2019-01-012019-04-230001743745us-gaap:NoncontrollingInterestMember2019-01-012019-04-230001743745us-gaap:CommonClassAMember2019-01-012019-04-230001743745us-gaap:CommonClassBMember2019-01-012019-04-230001743745us-gaap:CommonClassCMember2019-01-012019-04-230001743745us-gaap:RetainedEarningsMember2019-04-242019-12-310001743745us-gaap:NoncontrollingInterestMember2019-04-242019-12-3100017437452019-04-242019-12-310001743745us-gaap:AdditionalPaidInCapitalMember2019-04-242019-12-310001743745us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-04-242019-12-310001743745us-gaap:CommonClassAMember2019-04-242019-12-310001743745us-gaap:CommonClassBMember2019-04-242019-12-310001743745gnln:RedeemableClassBUnitsMember2019-12-310001743745gnln:MembersEquityMember2019-12-310001743745us-gaap:AdditionalPaidInCapitalMember2019-12-310001743745us-gaap:RetainedEarningsMember2019-12-310001743745us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310001743745us-gaap:NoncontrollingInterestMember2019-12-310001743745us-gaap:RetainedEarningsMember2020-01-012020-12-310001743745us-gaap:NoncontrollingInterestMember2020-01-012020-12-310001743745us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001743745us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001743745us-gaap:CommonClassAMember2020-01-012020-12-310001743745us-gaap:AdditionalPaidInCapitalMemberus-gaap:CommonClassAMember2020-01-012020-12-310001743745us-gaap:CommonClassBMember2020-01-012020-12-310001743745us-gaap:CommonClassCMember2020-01-012020-12-310001743745gnln:RedeemableClassBUnitsMember2020-12-310001743745gnln:MembersEquityMember2020-12-310001743745us-gaap:AdditionalPaidInCapitalMember2020-12-310001743745us-gaap:RetainedEarningsMember2020-12-310001743745us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001743745us-gaap:NoncontrollingInterestMember2020-12-310001743745us-gaap:CommonClassAMemberus-gaap:IPOMember2019-04-232019-04-230001743745gnln:CommonStockClassAMemberus-gaap:IPOMember2019-04-232019-04-230001743745gnln:CommonStockClassAMember2019-04-230001743745gnln:CommonStockClassAMember2020-01-012020-12-31xbrli:pure0001743745gnln:CommonStockClassAMember2019-04-292019-04-290001743745gnln:ClassBCommonStockMember2020-01-012020-12-310001743745gnln:ClassCCommonStockMember2020-01-012020-12-310001743745gnln:PublicPurchasersMember2020-01-012020-12-310001743745us-gaap:CommonClassAMembergnln:PublicPurchasersMember2020-01-012020-12-310001743745gnln:NonFounderMembersMemberus-gaap:CommonClassBMember2020-01-012020-12-310001743745gnln:FounderMembersMemberus-gaap:CommonClassCMember2020-01-012020-12-310001743745gnln:AirgraftIncMember2020-12-3100017437452019-04-300001743745gnln:BillAndHoldMember2020-01-012020-12-310001743745gnln:AirgraftIncMemberus-gaap:IPOMember2020-01-012020-12-310001743745gnln:AirgraftIncMemberus-gaap:IPOMember2020-12-310001743745gnln:AirgraftIncMemberus-gaap:IPOMember2019-12-310001743745gnln:MintProductsMemberus-gaap:SalesRevenueNetMemberus-gaap:ProductConcentrationRiskMember2020-01-012020-12-310001743745gnln:MintProductsMemberus-gaap:SalesRevenueNetMemberus-gaap:ProductConcentrationRiskMember2019-01-012019-12-310001743745us-gaap:SalesRevenueNetMemberus-gaap:ProductConcentrationRiskMembergnln:ProductsWithoutPMTAMember2020-01-012020-12-310001743745us-gaap:SalesRevenueNetMemberus-gaap:ProductConcentrationRiskMembergnln:ProductsWithoutPMTAMember2019-01-012019-12-3100017437452020-10-012020-12-3100017437452020-01-010001743745us-gaap:AccountingStandardsUpdate201602Member2019-01-010001743745gnln:PollenGearLLCMember2019-01-140001743745gnln:ConsciousWholesaleMember2019-09-300001743745gnln:ConsciousWholesaleMember2019-09-302019-09-300001743745gnln:ConsciousWholesaleMember2019-10-012019-12-310001743745gnln:ConsciousWholesaleMember2020-01-012020-12-310001743745gnln:ConsciousWholesaleMember2019-12-310001743745gnln:ConsciousWholesaleMemberus-gaap:TradeNamesMember2019-10-012019-12-310001743745us-gaap:CustomerRelationshipsMembergnln:ConsciousWholesaleMember2019-10-012019-12-310001743745gnln:PollenGearLLCMember2019-01-012019-12-310001743745us-gaap:FairValueInputsLevel1Member2020-12-310001743745us-gaap:FairValueInputsLevel2Member2020-12-310001743745us-gaap:FairValueInputsLevel3Member2020-12-310001743745us-gaap:FairValueInputsLevel1Member2019-12-310001743745us-gaap:FairValueInputsLevel2Member2019-12-310001743745us-gaap:FairValueInputsLevel3Member2019-12-310001743745us-gaap:InterestRateSwapMember2020-12-310001743745gnln:ConsciousWholesaleMemberus-gaap:FairValueInputsLevel3Member2018-12-310001743745us-gaap:LongTermDebtMemberus-gaap:FairValueInputsLevel3Member2018-12-310001743745us-gaap:LongTermDebtMemberus-gaap:FairValueInputsLevel3Member2019-01-012019-12-310001743745gnln:ConsciousWholesaleMemberus-gaap:FairValueInputsLevel3Member2019-01-012019-12-310001743745gnln:ConsciousWholesaleMemberus-gaap:FairValueInputsLevel3Member2019-12-310001743745us-gaap:LongTermDebtMemberus-gaap:FairValueInputsLevel3Member2019-12-310001743745gnln:ConsciousWholesaleMemberus-gaap:FairValueInputsLevel3Member2020-01-012020-12-310001743745gnln:ConsciousWholesaleMemberus-gaap:FairValueInputsLevel3Member2020-12-310001743745us-gaap:LongTermDebtMemberus-gaap:FairValueInputsLevel3Member2020-12-31gnln:facility0001743745srt:MinimumMemberus-gaap:BuildingMember2020-12-310001743745us-gaap:BuildingMembersrt:MaximumMember2020-12-310001743745country:US2020-12-310001743745srt:MinimumMember2020-12-310001743745srt:MaximumMember2020-12-310001743745us-gaap:NotesPayableOtherPayablesMember2020-12-310001743745us-gaap:NotesPayableOtherPayablesMember2019-12-310001743745us-gaap:LetterOfCreditMember2020-12-310001743745us-gaap:LetterOfCreditMember2019-12-310001743745us-gaap:LetterOfCreditMember2018-10-012018-10-010001743745us-gaap:LetterOfCreditMember2019-04-052019-04-050001743745us-gaap:RealEstateLoanMember2018-10-010001743745us-gaap:ConvertibleDebtMember2018-12-310001743745us-gaap:ConvertibleDebtMember2018-12-012018-12-310001743745us-gaap:ConvertibleDebtMember2019-01-310001743745us-gaap:ConvertibleDebtMember2019-01-012019-01-310001743745us-gaap:ConvertibleDebtMember2019-01-012019-03-3100017437452019-04-012019-04-300001743745us-gaap:MachineryAndEquipmentMember2020-01-012020-12-310001743745us-gaap:MachineryAndEquipmentMember2020-12-310001743745gnln:FurnitureEquipmentAndSoftwareMember2020-12-310001743745gnln:FurnitureEquipmentAndSoftwareMember2019-12-310001743745srt:MinimumMembergnln:FurnitureEquipmentAndSoftwareMember2020-01-012020-12-310001743745gnln:FurnitureEquipmentAndSoftwareMembersrt:MaximumMember2020-01-012020-12-310001743745gnln:PersonalPropertyMember2020-12-310001743745gnln:PersonalPropertyMember2019-12-310001743745gnln:PersonalPropertyMember2020-01-012020-12-310001743745us-gaap:LeaseholdImprovementsMember2020-12-310001743745us-gaap:LeaseholdImprovementsMember2019-12-310001743745us-gaap:LeaseholdImprovementsMember2020-01-012020-12-310001743745us-gaap:LandImprovementsMember2020-12-310001743745us-gaap:LandImprovementsMember2019-12-310001743745us-gaap:LandImprovementsMember2020-01-012020-12-310001743745us-gaap:BuildingMember2020-12-310001743745us-gaap:BuildingMember2019-12-310001743745us-gaap:BuildingMember2020-01-012020-12-310001743745us-gaap:LandMember2020-12-310001743745us-gaap:LandMember2019-12-310001743745gnln:WorkInProcessMember2020-12-310001743745gnln:WorkInProcessMember2019-12-310001743745gnln:DesignLibrariesMember2020-12-310001743745gnln:DesignLibrariesMember2020-01-012020-12-310001743745us-gaap:TrademarksAndTradeNamesMember2020-12-310001743745srt:MinimumMemberus-gaap:TrademarksAndTradeNamesMember2020-01-012020-12-310001743745srt:MinimumMemberus-gaap:TrademarksAndTradeNamesMember2019-01-012019-12-310001743745srt:MaximumMemberus-gaap:TrademarksAndTradeNamesMember2020-01-012020-12-310001743745srt:MaximumMemberus-gaap:TrademarksAndTradeNamesMember2019-01-012019-12-310001743745us-gaap:CustomerRelationshipsMember2020-12-310001743745srt:MinimumMemberus-gaap:CustomerRelationshipsMember2019-01-012019-12-310001743745srt:MinimumMemberus-gaap:CustomerRelationshipsMember2020-01-012020-12-310001743745us-gaap:CustomerRelationshipsMembersrt:MaximumMember2019-01-012019-12-310001743745us-gaap:CustomerRelationshipsMembersrt:MaximumMember2020-01-012020-12-310001743745us-gaap:OtherIntangibleAssetsMember2020-12-310001743745srt:MinimumMemberus-gaap:OtherIntangibleAssetsMember2020-01-012020-12-310001743745srt:MinimumMemberus-gaap:OtherIntangibleAssetsMember2019-01-012019-12-310001743745us-gaap:OtherIntangibleAssetsMembersrt:MaximumMember2019-01-012019-12-310001743745us-gaap:OtherIntangibleAssetsMembersrt:MaximumMember2020-01-012020-12-310001743745gnln:DesignLibrariesMember2019-12-310001743745gnln:DesignLibrariesMember2019-01-012019-12-310001743745us-gaap:TrademarksAndTradeNamesMember2019-12-310001743745us-gaap:CustomerRelationshipsMember2019-12-310001743745us-gaap:OtherIntangibleAssetsMember2019-12-310001743745us-gaap:TrademarksAndTradeNamesMember2020-01-012020-12-310001743745us-gaap:OtherIntangibleAssetsMember2020-01-012020-12-3100017437452020-01-012020-03-310001743745country:US2019-12-310001743745country:CA2019-12-310001743745srt:EuropeMember2019-12-310001743745country:US2020-01-012020-12-310001743745country:CA2020-01-012020-12-310001743745srt:EuropeMember2020-01-012020-12-310001743745country:CA2020-12-310001743745srt:EuropeMember2020-12-310001743745us-gaap:AccumulatedTranslationAdjustmentMember2018-12-310001743745us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2018-12-310001743745us-gaap:AccumulatedTranslationAdjustmentMember2019-01-012019-12-310001743745us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2019-01-012019-12-310001743745us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001743745us-gaap:AccumulatedTranslationAdjustmentMember2019-12-310001743745us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2019-12-310001743745us-gaap:AccumulatedTranslationAdjustmentMember2020-01-012020-12-310001743745us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2020-01-012020-12-310001743745us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310001743745us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2020-12-310001743745gnln:VendorOneMemberus-gaap:SupplierConcentrationRiskMember2020-01-012020-12-310001743745gnln:VendorTwoMemberus-gaap:SupplierConcentrationRiskMember2020-01-012020-12-310001743745gnln:VendorOneMemberus-gaap:SupplierConcentrationRiskMember2019-01-012019-12-310001743745gnln:VendorTwoMemberus-gaap:SupplierConcentrationRiskMember2019-01-012019-12-3100017437452019-04-170001743745us-gaap:CommonClassAMember2019-04-170001743745us-gaap:CommonClassBMember2019-04-170001743745us-gaap:CommonClassCMember2019-04-1700017437452019-04-172019-04-170001743745us-gaap:CommonClassAMemberus-gaap:IPOMember2019-04-012019-04-230001743745gnln:CommonStockClassAMemberus-gaap:IPOMember2019-04-012019-04-230001743745gnln:CommonStockClassAMemberus-gaap:IPOMember2019-04-2300017437452019-11-300001743745us-gaap:CommonClassAMember2019-01-012019-12-310001743745us-gaap:StockOptionMember2020-01-012020-12-310001743745us-gaap:CommonClassBMember2019-01-012019-12-310001743745gnln:ClassCCommonStockMember2019-01-012019-12-310001743745us-gaap:StockOptionMember2019-01-012019-12-310001743745gnln:TwoThousandNineteenEquityIncentivePlanMember2020-12-310001743745us-gaap:IPOMember2020-01-012020-12-310001743745srt:MinimumMemberus-gaap:IPOMember2020-12-310001743745srt:MaximumMemberus-gaap:IPOMember2020-12-310001743745srt:MinimumMember2020-01-012020-12-310001743745srt:MaximumMember2020-01-012020-12-310001743745us-gaap:IPOMember2019-01-012019-12-310001743745srt:MinimumMemberus-gaap:IPOMember2019-12-310001743745srt:MaximumMemberus-gaap:IPOMember2019-12-310001743745srt:MinimumMember2019-01-012019-12-310001743745srt:MaximumMember2019-01-012019-12-310001743745us-gaap:EmployeeStockOptionMemberus-gaap:EmployeeStockMember2020-01-012020-12-310001743745us-gaap:EmployeeStockOptionMemberus-gaap:EmployeeStockMember2019-01-012019-12-310001743745us-gaap:RestrictedStockMember2020-01-012020-12-310001743745us-gaap:CommonStockMember2020-01-012020-12-310001743745us-gaap:StateAndLocalJurisdictionMember2020-12-310001743745us-gaap:ForeignCountryMember2020-12-310001743745srt:ReportableGeographicalComponentsMembercountry:US2020-01-012020-12-310001743745srt:ReportableGeographicalComponentsMembercountry:US2019-01-012019-12-310001743745srt:ReportableGeographicalComponentsMembercountry:CA2020-01-012020-12-310001743745srt:ReportableGeographicalComponentsMembercountry:CA2019-01-012019-12-310001743745srt:ReportableGeographicalComponentsMembersrt:EuropeMember2020-01-012020-12-310001743745srt:ReportableGeographicalComponentsMembersrt:EuropeMember2019-01-012019-12-310001743745us-gaap:CorporateNonSegmentMember2020-01-012020-12-310001743745us-gaap:CorporateNonSegmentMember2019-01-012019-12-310001743745srt:ReportableGeographicalComponentsMembercountry:US2020-12-310001743745srt:ReportableGeographicalComponentsMembercountry:US2019-12-310001743745srt:ReportableGeographicalComponentsMembercountry:CA2020-12-310001743745srt:ReportableGeographicalComponentsMembercountry:CA2019-12-310001743745srt:ReportableGeographicalComponentsMembersrt:EuropeMember2020-12-310001743745srt:ReportableGeographicalComponentsMembersrt:EuropeMember2019-12-310001743745us-gaap:CorporateNonSegmentMember2020-12-310001743745us-gaap:CorporateNonSegmentMember2019-12-310001743745gnln:VaporizerAndComponentsMember2020-01-012020-12-310001743745gnln:VaporizerAndComponentsMember2019-01-012019-12-310001743745gnln:CustomProductsAndPackagingMember2020-01-012020-12-310001743745gnln:CustomProductsAndPackagingMember2019-01-012019-12-310001743745gnln:FunctionalAndGlassMember2020-01-012020-12-310001743745gnln:FunctionalAndGlassMember2019-01-012019-12-310001743745gnln:ToolsAndAppliancesMember2020-01-012020-12-310001743745gnln:ToolsAndAppliancesMember2019-01-012019-12-310001743745gnln:PartsAccessoriesAndCBDMember2020-01-012020-12-310001743745gnln:PartsAccessoriesAndCBDMember2019-01-012019-12-310001743745gnln:ClosedSystemMember2020-01-012020-12-310001743745gnln:ClosedSystemMember2019-01-012019-12-310001743745gnln:GrindersMember2020-01-012020-12-310001743745gnln:GrindersMember2019-01-012019-12-310001743745gnln:PapersAndWrapsMember2020-01-012020-12-310001743745gnln:PapersAndWrapsMember2019-01-012019-12-310001743745gnln:OtherMember2020-01-012020-12-310001743745gnln:OtherMember2019-01-012019-12-310001743745country:US2019-01-012019-12-310001743745country:CA2019-01-012019-12-310001743745srt:EuropeMember2019-01-012019-12-310001743745gnln:OtherMember2020-01-012020-12-310001743745gnln:OtherMember2019-01-012019-12-310001743745us-gaap:SubsequentEventMemberus-gaap:CommonClassBMember2021-01-012021-03-310001743745us-gaap:SubsequentEventMemberus-gaap:CommonClassCMember2021-01-012021-03-310001743745us-gaap:SubsequentEventMembergnln:EyceLLCMember2021-03-022021-03-020001743745us-gaap:SubsequentEventMembergnln:KushCoMember2021-01-012021-03-310001743745us-gaap:SubsequentEventMemberus-gaap:CommonClassBMember2021-03-310001743745us-gaap:SubsequentEventMemberus-gaap:CommonClassAMember2021-03-310001743745us-gaap:SubsequentEventMember2021-01-012021-03-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

001-38875

(Commission file number)

Greenlane Holdings, Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 83-0806637 |

State or other jurisdiction of

incorporation or organization | | (I.R.S. Employer

Identification No.) |

| | | | | | | | | | | |

| 1095 Broken Sound Parkway, | Suite 300 | | |

| Boca Raton, | FL | | 33487 |

| (Address of principal executive offices) | | (Zip Code) |

(877) 292-7660

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Class A Common Stock, $0.01 par value per share | | GNLN | | Nasdaq Global Market |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No £

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

Large accelerated filer | £ | Accelerated filer | £ |

Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| | Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the common equity held by non-affiliates of the registrant as of June 30, 2020, the last business day of the registrant's most recently completed second fiscal quarter, was approximately $48.8 million based upon the closing price reported for such date on the Nasdaq Global Select Market.

As of March 26, 2021, Greenlane Holdings, Inc. had 16,341,897 shares of Class A common stock outstanding, 2,443,437 shares of Class B common stock outstanding and 72,064,218 shares of Class C common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Proxy Statement for the 2020 Annual Meeting of Stockholders are incorporated herein by reference in Part III of this Form 10-K to the extent stated herein. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant's fiscal year ended December 31, 2020.

Greenlane Holdings, Inc.

Form 10-K

For the Fiscal Year Ended December 31, 2020

TABLE OF CONTENTS

| | | | | | | | |

| | Page |

| |

| | |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | |

PART III | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| PART IV | | |

| Item 15. | | |

| Item 16. | | |

| Signatures | |

NOTE ABOUT FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K ("Form 10-K") contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. Many of the forward-looking statements are located in Part, Item 7 of this Form 10-K under the heading "Management's Discussion and Analysis of Financial Condition and Results of Operations." Forward-looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact. In some cases, you can identify forward-looking statements by terminology such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could” and similar expressions. Examples of forward-looking statements include, without limitation:

•the impacts of the novel coronavirus ("COVID-19") pandemic and measures intended to prevent or mitigate its spread, and our ability to accurately assess and predict such impacts on our results of operations, financial condition, acquisition and disposition activities, and growth opportunities;

•statements regarding our growth and other strategies, results of operations or liquidity;

•statements concerning projections, predictions, expectations, estimates or forecasts as to our business, financial and operational results and future economic performance;

•statements regarding our industry;

•statements of management’s goals and objectives;

•projections of revenue, earnings, capital structure and other financial items;

•assumptions underlying statements regarding us or our business; and

•other similar expressions concerning matters that are not historical facts.

Forward-looking statements should not be read as a guarantee of future performance or results and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time those statements are made or management’s good faith belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to, those discussed in Part I, Item 1A of this Form 10-K under the heading “Risk Factors" and in other documents that we file from time to time with the Securities and Exchange Commission (the "SEC").

Forward-looking statements involve estimates, assumptions, known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from any future results, performances, or achievements expressed or implied by the forward-looking statements. These risks include, but are not limited to, those listed below and those discussed in greater detail in Part I, Item 1A of this Form 10-K under the heading “Risk Factors."

•our strategy, outlook and growth prospects;

•general economic trends and trends in the industry and markets in which we operate;

•public heath crises, including the COVID-19 pandemic;

•our dependence on, and our ability to establish and maintain business relationships with, third-party suppliers and service suppliers;

•the competitive environment in which we operate;

•our vulnerability to third-party transportation risks;

•the impact of governmental laws and regulations and the outcomes of regulatory or agency proceedings;

•our ability to accurately estimate demand for our products and maintain appropriate levels of inventory;

•our ability to maintain or improve our operating margins and meet sales expectations;

•our ability to adapt to changes in consumer spending and general economic conditions;

•our ability to use or license certain trademarks;

•our ability to maintain consumer brand recognition and loyalty of our products;

•our and our customers’ ability to establish or maintain banking relationships;

•fluctuations in U.S. federal, state, local and foreign tax obligation and changes in tariffs;

•our ability to address product defects;

•our exposure to potential various claims, lawsuits and administrative proceedings;

•contamination of, or damage to, our products;

•any unfavorable scientific studies on the long-term health risks of vaporizers, electronic cigarettes, e-liquids products or hemp-derived products, including cannabidiol (“CBD”);

•failure of our information technology systems to support our current and growing business;

•our ability to prevent and recover from Internet security breaches;

•our ability to generate adequate cash from our existing business to support our growth;

•our ability to protect our intellectual property rights;

•our dependence on continued market acceptance of our products by consumers;

•our sensitivity to global economic conditions and international trade issues;

•our ability to comply with certain environmental, health and safety regulations;

•our ability to successfully identify and complete strategic acquisitions;

•natural disasters, adverse weather conditions, operating hazards, environmental incidents and labor disputes;

•increased costs as a result of being a public company; and

•our failure to maintain adequate internal controls over financial reporting.

Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition or operating results.

The forward-looking statements speak only as of the date on which they are made, and, except as required by law, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Consequently, you should not place undue reliance on forward-looking statements.

Summary Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may materially and adversely affect our business, financial condition, results of operations, cash flows and prospects. These risks are discussed more fully in Item 1A. Risk Factors herein. These risks include, but are not limited to, the following:

•We have at times experienced rapid growth, both domestically and internationally, and expect continued future growth, including growth from additional acquisitions. If we fail to manage our growth effectively, we may be unable to execute our business plan, maintain high levels of service or address competitive challenges adequately. Furthermore, our corporate culture has contributed to our success, and if we cannot maintain this culture as we grow, we could lose the innovation, creativity, and teamwork fostered by our culture, and our business may be harmed.

•The market for vaporizer products and related items is a niche market, subject to a great deal of uncertainty and is still evolving.

•We depend on third-party suppliers for our products and may experience unexpected supply shortages.

•A significant percentage of our revenue is dependent on sales of products from a relatively small number of key suppliers, and a decline in sales of products from these suppliers could materially harm our business.

•The FDA has expressed growing concern about the popularity among youth of the products of JUUL Labs and other manufactures of ENDS products and has imposed significant regulation on ENDS products. Additional regulatory actions may further impact our ability to sell these products in the United States or online.

•There is uncertainty related to the regulation of vaporization products and certain other consumption accessories at all levels of government. Significant increases in state and local regulation of our vaporizer products have been proposed and enacted, and are likely to continue to be proposed and enacted in numerous jurisdictions. Increased regulatory compliance burdens could have a material adverse impact on our business development efforts and our operations.

•Demand for the products we distribute could decrease if the suppliers of these products were to substantially the amount of goods sold directly to consumers in the sectors we serve.

•We may not be able to maintain existing supplier relationships or exclusive distributor status with our suppliers, which may affect our ability to offer a broad selection of products at competitive prices and negatively impact our results of operations.

•We do not have long-term contracts with most of our customers. The agreements that we do have generally do not commit our customers to any minimum purchase volume. The loss of a significant customer may have a material adverse effect on us.

•Because a majority of our revenues are derived from sales to consumers indirectly through third-party retailers who operate traditional brick-and-mortar locations, the shift of sales to more online retail business could harm our market share and our revenues in certain sectors.

•We may not be successful in maintaining the consumer brand recognition and loyalty of our products.

•Some of the products we sell contain nicotine, which is considered to be a highly-addictive substance, or other chemicals that some jurisdictions have determined to cause cancer and birth defects or other reproductive harm.

•Public health epidemics, pandemics or outbreaks, including the recent COVID-19 pandemic, could adversely affect our business.

•Our business depends partly on continued purchases by businesses and individuals selling or using cannabis pursuant to state laws in the United States or national and provincial laws in Canada.

•The federal and state regulatory landscape regarding products containing hemp-derived products is uncertain and evolving, and new or changing laws or regulations relating to hemp and hemp-derived products could have a material adverse effect on our business, financial condition and results of operations.

•We are subject to legislative uncertainty that could slow or halt the legalization and use of cannabis, which could negatively affect our business.

•Our business, and the business of the suppliers from which we acquire the products we sell, requires compliance with many laws and regulations in many jurisdictions globally across multiple product categories. Failure to comply with these laws and regulations could subject us or such suppliers to regulatory or agency proceedings, prosecutions, or investigations and could also lead to damage awards, fines and penalties.

•While we believe that our business and sales do not violate the Federal Paraphernalia Law, legal proceedings alleging violations of such law or changes in such law or interpretations thereof could materially and adversely affect our business, financial condition or results of operations.

•Officials of the U.S. Customs and Border Protection agency (“CBP”) have broad discretion regarding products imported into the United States, and the CBP has on occasion seized imported products on the basis that such products violate the Federal Paraphernalia Law. While we believe the products that we import do not violate such law, any such seizure of the products we sell could have a material adverse effect on our business operations or our results of operations.

•Because our business is dependent, in part, upon continued market acceptance of cannabis by consumers, any negative trends could materially and adversely affect our business, financial conditions or results of operations.

•Recently adopted laws prohibit the mailing of certain vaporizer products through the United States Postal Service (“USPS”) and place certain regulatory requirements on shipment of those products through other carriers. Additionally, carriers including UPS and FedEx have imposed policies restricting the shipment of vaporizers. If the products we carry cannot be shipped by the USPS or private carriers, or we must comply with burdensome policies and regulations, our shipping costs could increase materially and we could lose our ability to deliver products to customers in a timely and economical matter.

•We and our customers may have difficulty accessing the service of banks, which may make it difficult for us and for them to sell our products.

•The scientific community has not yet extensively studied the long-term health effects of the use of vaporizers, electronic cigarettes or e-liquids products.

•Two of our senior executives, Aaron LoCascio and Adam Schoenfeld, have control over all stockholder decisions because collectively they control a substantial majority of the voting power of our common stock. This will limit or preclude your ability to influence corporate matters, including the election of directors, amendments of our organizational documents and any merger, consolidation, sale of all or substantially all of our assets, or other major corporate transaction requiring stockholder approval.

•The market price of our Class A common stock has been volatile and has declined significantly since our initial public offering and may face more volatility and price declines in the future. As a result, you may not be able to resell your shares at or above the price at which you have acquired or will acquire shares of our Class A common stock.

•We have not paid dividends in the past and have no current plans to pay dividends in the future, and any return on investment may be limited to the value of our common stock.

PART I

ITEM 1. BUSINESS

General

We are one of the largest global sellers of premium cannabis accessories and liquid nicotine products in the world. We operate as a third-party brand accelerator, a powerful house of brands, and a distribution platform for consumption devices and lifestyle brands serving the global cannabis, hemp-derived CBD, and liquid nicotine markets. We have an established track record of partnering with brands through all stages of the product lifecycle, and serve an expansive customer base covering over 8,000 locations, which includes over 1,100 licensed cannabis businesses and 4,100 smoke and vape shops. We supply our products to stores around the globe, offering only the most desired, high-quality products.

We are the partner of choice for many of the industry’s leading players including PAX Labs, Grenco Science, Storz & Bickel, Firefly, DaVinci, Santa Cruz Shredder, Cookies, among others. We have also set out to develop a world-class portfolio of our own proprietary brands ("Greenlane Brands") that we believe, over time will, deliver higher margins and create long-term value. Our Greenlane Brands include VIBES Rolling Papers, Pollen Gear, the Marley Natural accessory line, Aerospaced & Groove grinders, K. Haring Glass Collections, and Higher Standards, which serves as both upscale product line and an innovative retail experience with flagship stores at New York City’s famed Chelsea Market and a location in California's iconic Malibu Village. Subsequent to December 31, 2020, we added Eyce to our Greenlane Brands lineup through the acquisition of substantially all of the assets of Eyce LLC effective March 2, 2021. We also own and operate several industry-leading e-commerce platforms, including Vapor.com, Higherstandards.com, Aerospaced.com, Canada.vapor.com and Vaposhop.com, among others. These e-commerce platforms offer our consumers a convenient and flexible shopping solution.

We have a diverse source of revenue from both business-to-business ("B2B") transactions through wholesale distribution to retailers and business-to-consumer ("B2C") transactions through e-commerce and brick-and-mortar retail sales in three geographically distinct operating segments, which include our United States, Canada, and European operations. For the years ended December 31, 2020 and 2019, sales generated by our United States operating segment accounted for approximately 81.3% and 86.6% of net sales, respectively. Total net sales generated by our Canadian operations for the years ended December 31, 2020 and 2019 accounted for approximately 11.2% and 12.0%, respectively, and our European operations accounted for approximately 7.5% and 1.4% of net sales over the same periods. European operations did not commence until completion of the Conscious Wholesale acquisition in September 2019; therefore, the 2019 results reflect only three months of net sales for this operating segment. Given the recency of the acquisition, we expect our European operating segment to continue increasing as a percentage of our consolidated net sales. Refer to "Note 11— Segment Reporting" within Item 8 for additional information on our reportable segments.

Our diversity in the source of our revenue is further apparent through our increasingly low customer concentration, with our top ten customers accounting for only 9.8% and 17.3% of our net sales for the years ended December 31, 2020 and 2019, respectively, and no single customer accounting for more than 10% of our net sales over the two-year period ended December 31, 2020. While we distribute our products to a number of large national and regional retailers in the United States, Canada and Europe, our typical B2B customer is an independent retailer operating in a single market. Our sales teams regularly interact with our customers, as most of them have frequent restocking needs. We believe our high-touch customer service model strengthens relationships, builds loyalty and drives repeat business. In addition, we believe our premium product lines, broad product portfolio and strategic distribution network position us well to meet the needs of our customers and ensure timely delivery of products.

For the year ended December 31, 2020, revenues derived from B2B, B2C, and Supply & Packaging ("S&P") transactions represented approximately 60.4%, 14.3%, and 11.5% of net sales, respectively, compared to approximately 78.1%, 5.9%, and 10.8%, respectively, of net sales for the same period in 2019. Channel sales and drop-ship revenues derived from the sales and shipment of our products to the customers of third-party website operations and providing other services to our customers represented approximately 13.8% of net sales for the year ended December 31, 2020, compared to approximately 5.2% for the same period in 2019.

Organization

Greenlane Holdings, Inc. (“Greenlane” and, collectively with the Operating Company (as defined below) and its consolidated subsidiaries, the “Company”, "we", "us" and "our") was formed as a Delaware corporation on May 2, 2018. We are a holding company that was formed for the purpose of completing an underwritten initial public offering (“IPO”) of shares of our Class A common stock on April 23, 2019 and other related transactions in order to carry on the business of Greenlane Holdings, LLC (the “Operating Company”). The Operating Company was organized under the laws of the state of Delaware on September 1, 2015, and is based in Boca Raton, Florida. Refer to "Note 1—Business Operations and Organizations" within Item 8 for further information on the Company's organization and the IPO and related transactions. We are the sole manager of the Operating Company and, as of December 31, 2020, owned a 31.6% interest in the Operating Company.

Our Business Relating to the Cannabis Industry

The information included below is based on the most recent information available to the Company and, except as expressly stated below, does not give effect to the continued impact of the COVID-19 pandemic; the long-term impacts of which remain uncertain as of the date of this Form 10-K.

While we do not cultivate, distribute or dispense marijuana as that term is defined by the Controlled Substances Act, several of the products we distribute, such as vaporizers, pipes, rolling papers and storage solutions, can be used with marijuana or marijuana derivatives, as well as several other legal substances.

We believe the global cannabis industry is experiencing a transformation from a state of prohibition toward a state of legalization. We expect the number of states, countries and other jurisdictions implementing legalization legislation to continue to increase, which will create numerous and sizable opportunities for market participants, including us.

Global Landscape

A September 2020 report of Arcview Market Research and BDS Analytics, two of the leading market research firms in the cannabis industry, estimated that spending in the global legal cannabis market was approximately $14.9 billion in 2019 and reached approximately $19.7 billion as of September 2020, representing growth of approximately 32.2%. The report projects that by 2025, spending in the global legal cannabis market will reach $47.2 billion, representing a compound annual growth rate of approximately 22% over the six-year period from 2019. Our experience and awareness of the markets in which we operate lead us to believe that demand for the types of products we distribute will grow in tandem with the industry.

The North American Cannabis Landscape

United States and Territories. Thirty-eight states and the District of Columbia have legalized medical cannabis in some form and have a formal cannabis program. Fifteen of these states, and the District of Columbia, have legalized cannabis for non-medical adult use with additional states, such as New York, actively considering the legalization of cannabis for non-medical adult use. Eleven additional states have legalized high CBD, low tetrahydrocannabinol ("THC") oils for a limited class of patients. Only three states continue to prohibit cannabis entirely. Notwithstanding the continued trend toward further state legalization, cannabis continues to be categorized as a Schedule I controlled substance under the Federal Controlled Substances Act (the “CSA”) and, accordingly, the cultivation, processing, distribution, sale and possession of cannabis violate federal law in the United States as discussed further in Item 1A under the heading "Risk Factors." Our business depends partly on continued purchases by businesses and individuals selling or using cannabis pursuant to state laws in the United States or Canadian and provincial laws.

We believe support for cannabis legalization in the United States is gaining momentum. According to an October 2020 poll by Gallup, public support for the legalization of cannabis in the United States has increased from approximately 12% in 1969 to approximately 68% in 2020. In 2020, five states passed ballot initiatives legalizing either adult use or medical cannabis, further evidencing the public's support for cannabis legalization U.S. legal cannabis sales are projected to represent approximately 73% of total global sales by 2025.

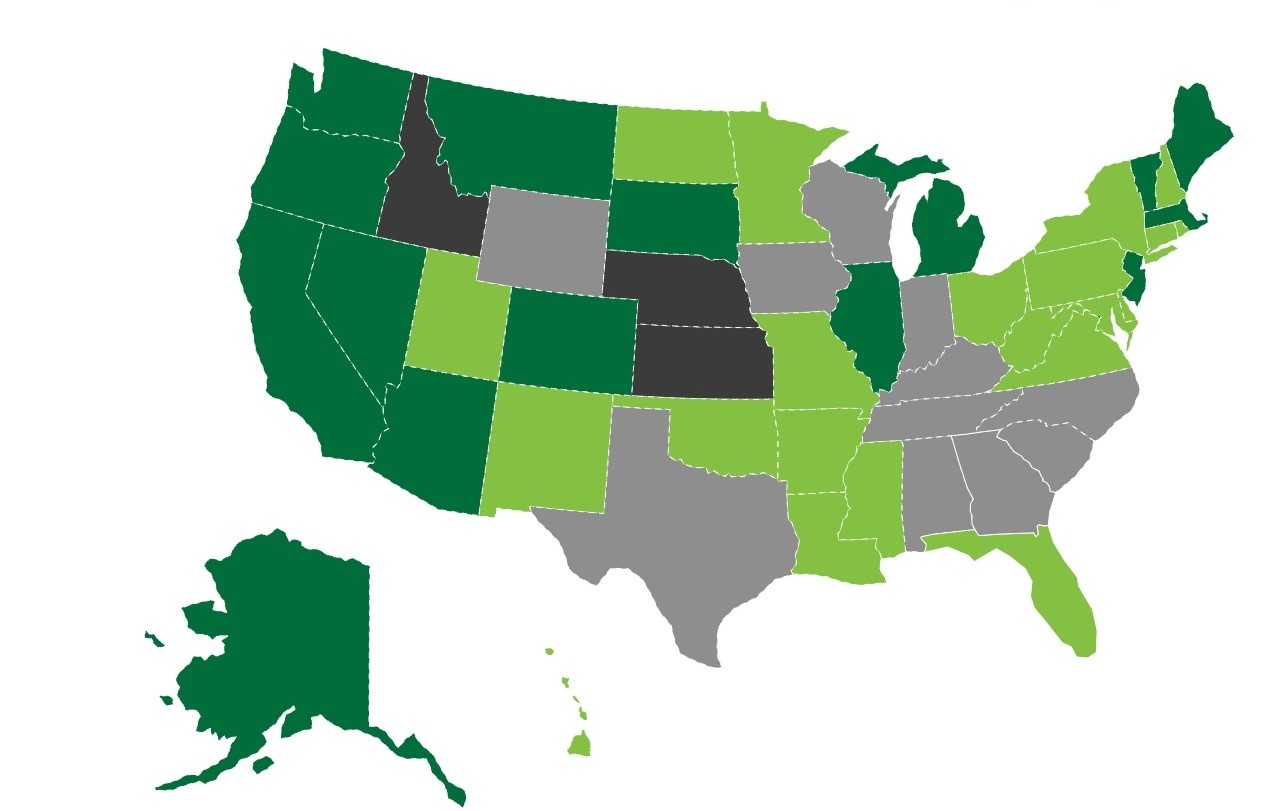

The following map from the National Cannabis Industry Association illustrates the states that have fully legalized adult-use cannabis (for medical and recreational purposes), states that have partially legalized cannabis (for medical purposes only), and states that have legalized cannabis use in a limited capacity (as of February 8, 2021).

U.S. CBD Landscape

In December 2018, the Farm Bill was signed into law in the United States which specifically removed hemp from the definition of “marijuana” under the Controlled Substances Act. In addition, the Farm Bill designated hemp as an agricultural commodity and permits the lawful cultivation of hemp in all states and territories of the United States. Federal and state laws and regulations concerning the cultivation and sale of hemp and hemp-derived products (including CBD) continue to evolve.

Canada.

Legal access to dried cannabis for medical purposes was first allowed in Canada in 1999. The Cannabis Act (the “Cannabis Act”) currently governs the production, sale and distribution of medical cannabis and related oil extracts in Canada.

On April 13, 2017, the Government of Canada introduced Bill C-45, which proposed the enactment of the Cannabis Act to legalize and regulate access to cannabis. The Cannabis Act proposed a strict legal framework for controlling the production, distribution, sale and possession of medical and recreational adult-use cannabis in Canada. On June 21, 2018, the Government of Canada announced that Bill C-45 received Royal Assent. On July 11, 2018, the Government of Canada published the Cannabis Regulations under the Cannabis Act. The Cannabis Regulations provide more detail on the medical and recreational regulatory regimes for cannabis, including regarding licensing, security clearances and physical security requirements, product practices, outdoor growing, security, packaging and labelling, cannabis-containing drugs, document retention requirements, reporting and disclosure requirements, the new access to cannabis for medical purposes regime and industrial hemp. The majority of the Cannabis Act and the Cannabis Regulations came into force on October 17, 2018, with additional Cannabis regulations coming into effect on October 17, 2019.

While the Cannabis Act provides for the regulation by the federal government of, among other things, the commercial cultivation and processing of cannabis for recreational purposes, it provides the provinces and territories of Canada with the authority to regulate in respect of the other aspects of recreational cannabis, such as distribution, sale, minimum age requirements, places where cannabis can be consumed, and a range of other matters.

The governments of every Canadian province and territory have implemented regulatory regimes for the distribution and sale of cannabis for recreational purposes. Most provinces and territories have announced a minimum age of 19 years old, except for Québec and Alberta, where the minimum age will be 18. Certain provinces, such as Ontario, have legislation in place that restricts the packaging of vapor products and the manner in which vapor products are displayed or promoted in stores.

The European Cannabis Landscape

Europe’s population is larger than that of the U.S. and Canadian markets combined, suggesting the potential of a very significant market. The changes in regulations for cannabis products across Europe are expected to result in a market growth of approximately $37.0 billion in annual sales by 2027, a significant growth from approximately $3.5 billion in 2020.

Currently, Germany, Italy, Austria, Czech Republic, Finland, Portugal, Spain, the Netherlands, Denmark, Greece, Croatia, North Macedonia, Poland, Turkey, Malta, Romania, Belgium, Estonia, Lithuania, Moldova, Norway, San Marino, Sweden, Switzerland, Luxembourg, Cyprus, France, the U.K and Ireland allow cannabis use for medicinal purposes, with some of those countries operating pilot programs. It has been widely reported that other countries are considering following suit.

Product Information

Consumers of cannabis, herbs, flavored compounds, aromatherapy oils and nicotine require the types of products we distribute, including vaporizers, pipes, rolling papers and packaging. We believe we distribute the “picks & shovels” for these rapidly-growing industries. As the world of cannabis and its respective aesthetic continues to expand, we strive to keep our product mix relevant, popular, and innovative; offering an array of products from vaporizers, grinders, to rolling papers and apparel lines. As our product offerings continue to develop and expand, we expect our revenue by categories to increase accordingly.

Inhalation Delivery Methods

There are two prevalent types of inhalation methods for cannabis and nicotine: combustion and vaporization. Vaporizers are devices that heat materials to temperatures below the point of combustion, extracting the flavors, aromas and effects of dry herbs and concentrates in the form of vapor. Measured by revenue, vaporizers are our largest product category.

The Science and Popularity of Vaporization

Vaporizers have elements that are designed to quickly heat material, causing vaporization to occur without the carbon dioxide that is typically generated through any combustion. The vapor byproduct is then immediately inhaled through the mouthpiece on the device itself, or through a hose or an inflatable bag. Vaporizers can heat a variety of dry materials, viscous liquids and waxes, and provide a convenient way for users to consume the active ingredients. Common ingredients used in vaporizers include tobacco, nicotine extracts, legal herbs, hemp-derived CBD, aromatherapy oils, cannabis and propylene glycol and glycerin blends.

Vaporization Technology. Consumers have a wide array of vaporization devices at their disposal, which can be broadly categorized into two primary categories: desktop and portable vaporizers. Our vaporizer offering spans over 260 distinct products across 90 brands.

Desktop Vaporizers. Vaporizers were first developed as desktop models that were powered through traditional electric power sources. Desktop vaporizers are capable of heating the material to a more precise temperature choice determined by the consumer or as advised by a health practitioner. Some models dispense the vapor through a pipe or wand, and others into an inflatable bag in order to allow users to more accurately monitor their consumption.

Portable Vaporizers. With the development of lithium batteries, vaporizers have now become portable. Technological advances are resulting in lighter, sleeker and more visually-appealing units that are capable of quickly heating the material to the user’s desired temperature setting. The temperature setting can be fixed by the manufacturer or set manually by the consumer or via Bluetooth connection to the consumer’s smartphone. Portable vaporizers, of which pens are a sub-set, are differentiated by many features, including output, battery life, recharge time, material, capacity and design.

Other Methods of Consumption. In addition to vaporizers, consumers have a wide array of methods of consumption at their disposal, including, among others, hand pipes, water pipes, rolling papers, and oral and topical delivery methods.

Hand and Water Pipes. We offer a diverse portfolio of over 200 hand and water pipes across 27 brands, including our own proprietary Higher Standards, Marley Natural and K. Haring Glass brands. Many display iconic, licensed logos and artwork, as pipes have grown into an artistic expression and are available in countless creative forms and functionality. Hand pipes are small, portable and simple to use, and function by trapping the smoke produced from burning materials, which is then inhaled by the user. Water pipes include large table-top models, bubblers and rigs, and are more complex because they incorporate the cooling effects of water to the burning materials before inhalation.

Rolling Papers. Rolling papers are a traditional consumption method used to smoke dried plant material in a "roll-your-own" application. These include papers, cones and wraps. Our rolling papers category is comprised of over 100 products across 17 brands, inclusive of Greenlane Brand's own Vibes Rolling Papers brand, not including accessories such as rolling trays or tips.

Our Competitive Strengths

We attribute our success to the following competitive strengths:

A Clear Market Leader in an Attractive Industry.

We are a leading North American distributor of premium vaporization products and consumption accessories, reaching over 1,000 licensed cannabis cultivators, processors and dispensaries. We also own and operate one of the industry’s most visited North American direct-to-consumer e-commerce websites, Vapor.com. Vapor.com was launched in April 2019 when we consolidated our previously owned websites, Vapeworld.com and Vapornation.com, into one homogeneous website. The latter website, VaporNation, was acquired as part of our February 2019 purchase of Better Life Holdings, LLC. We also own and operate several industry-leading e-commerce platforms, including Higherstandards.com, Aerospaced.com, Vaposhop.com, and most recently Eycemolds.com.

Market Knowledge and Understanding.

Because of our experience and our extensive, long-term industry relationships, we believe we have a deep understanding of customer needs and desires in our B2B, B2C and S&P channels. This allows us to influence customer demand and the pipeline between product manufacturers, suppliers, advertisers and the marketplace.

Broadest Product Offering.

We believe we offer the industry’s most comprehensive portfolio of vaporization products and consumption accessories with over 5,000 SKUs (stock-keeping units) from more than 300 suppliers. This broad product offering creates a “one-stop shop" for our customers and positively distinguishes us from our competitors. In addition, we have carefully cultivated a portfolio of well-known brands and premium products and have helped many of the brands we distribute to become established names in the industry.

Entrepreneurial Culture.

We believe our entrepreneurial, results-driven culture fosters highly-dedicated employees who provide our customers with superior service. We invest in our talent by providing every sales representative with an extensive and ongoing education, and have successfully developed programs that provide comprehensive product knowledge and the tools needed to have a unique understanding of our customers’ personalities and decision-making processes.

Customers. We believe we offer superior services and solutions due to our comprehensive product offering, proprietary industry data and analytics, product expertise and quality of service. We deliver products to our customers in a precise, safe and timely manner with complementary support from our dedicated sales and service teams.

Suppliers. Our industry knowledge, market reach and resources allow us to establish trusted professional relationships with many of our product suppliers. We generate substantially all of our net sales from products manufactured by others. We have strong relationships with many large, well-established suppliers, and seek to establish distribution relationships with smaller or more recently established manufacturers in our industry. While we purchase our products from over 300 suppliers, a significant percentage of our net sales is dependent on sales of products from a small number of key suppliers. We believe there is a trend of suppliers in our industry to consolidate their relationships to do more business with fewer distributors. We believe our ability to help maximize the value and extend the distribution of our suppliers’ products has allowed us to benefit from this trend. The efforts of our senior management team have been integral to our relationships with our suppliers.

Employees. We provide our employees with an entrepreneurial culture, a safe work environment, financial incentives and career development opportunities.

Experienced and Proven Management Team Driving Organic and Acquisition Growth.

We believe our management team is among the most experienced in the industry. Our senior management team brings experience in accounting, mergers and acquisitions, financial services, consumer-packaged goods, retail operations, third-party logistics, information technology, product development and specialty retail, and an understanding of the cultural nuances of the industry that we serve.

Our Operating Strategies

We intend to leverage our competitive strengths to increase shareholder value through the following core strategies:

Build Upon Strong Customer and Supplier Relationships to Expand Organically.

Our North American footprint and broad supplier relationships, combined with our regular interaction with our large and diverse customer base, provides us key insights and positions us to be a critical link in the supply chain for premium vaporization products and consumption accessories. Our suppliers benefit from access to more than 8,000 brick and mortar locations and more than 1.8 million B2C customers, as we are a single point of contact for improved production, planning and efficiency. Our customers, in turn, benefit from our market leadership, talented sales associates, broad product offerings, high inventory availability, timely delivery and exceptional customer services. We believe our strong customer and supplier relationships will enable us to expand and broaden our market share in the premium vaporization products and consumption accessories marketplace and expand into new categories. For example, in November 2020, we entered into a partnership with Studenglass, which brought the Gravity Hookah to consumers and wholesale purchasers in the United States, Canada, and Europe.

Expand Our Operations Internationally.

We currently focus our marketing and sales efforts on the United States, Canada, and Europe, with the United States and Canada representing the two largest and most developed markets for our products. While we currently support and ship certain products to customers in Australia and parts of South America on a limited basis, we are aware of the growth opportunities in these markets. As we continue to expand our marketing, supplier relationships, sales bandwidth and expertise, we anticipate capturing market share in those regions by opening our own distribution centers, acquiring existing international distributors and/or partnering with local operators. In September 2019, we acquired Conscious Wholesale, a leading European wholesaler and retailer of consumption accessories, vaporizers, and other high-quality products. We assumed control of their existing warehouse facility located in Amsterdam, Netherlands, which is expected to facilitate the expansion of our European operations.

In February 2021, we opened three new Higher Standards shop-in-shop retail locations in Uruguay in a collaboration with the Kaya Herb Group. Further expanding Greenlane’s global footprint, these high-profile locations mark our first physical footprint in the South American market.

Expand our E-Commerce Reach and Capabilities.

We own and operate one of the leading direct-to-consumer e-commerce websites in our industry, Vapor.com. This site is one of the most visited within our industry according to SEMrush, a leading data analytics firm, and as of December 31, 2020, we ranked in the top five in 58 key mobile search terms and in the top ten in 93 key mobile search terms, On desktop computer searches, we ranked in the top five in 54 key search terms, and in the top ten in 96 key search terms. We recently expanded our E-Commerce platform into Canada through the launch of "Canada.Vapor.com" on October 26, 2020. Refer to Item 7 - Results of Operations for further detail on Canada.Vapor.com.

Pursue Value-Enhancing Strategic Acquisitions.

Through our acquisitions of VaporNation (Better Life Holdings, LLC), Pollen Gear LLC, and Conscious Wholesale, we have added new markets within the United States and Europe, new product lines, talented employees and operational best practices. Effective March 2, 2021, we acquired substantially all the assets of Eyce LLC, which further diversified our Greenlane Brand offerings through the integration of Eyce premium silicon smoking products and accessories. We intend to continue pursuing strategic acquisitions to grow our market share and enhance leadership positions by taking advantage of our scale, operational experience and acquisition know-how to pursue and integrate attractive targets. We believe we have significant opportunities to add product categories through our knowledge of our industry and possible acquisition targets.

Enhance Our Operating Margins.

We expect to enhance our operating margins as our business expands through a combination of additional product purchasing discounts, reduced inbound and outbound shipping and handling rates, reduced transaction processing fees, increased operating efficiencies and realization of benefits through leveraging our existing assets and distribution facilities. Additionally, we expect that our operating margins will increase as our product mix continues to evolve to include a greater portion of our proprietary branded products. We are committed to supporting our proprietary brands, such as Higher Standards, VIBES and Pollen Gear, which offer significantly higher gross margins than supplier-branded products.

Developing A World-Class Portfolio of Proprietary Brands.

We intend to continue to develop a portfolio of our own proprietary brands, which over time has helped to improve our blended margins and create long-term value. Our brand development is based upon our proprietary industry intelligence that allows us to identify market opportunities for new brands and products. We leverage our distribution infrastructure and

customer relationships to penetrate the market quickly with our proprietary brands and to gain placement in thousands of stores. Currently, we sell such products directly to consumers through our brand websites and our e-commerce properties. Our existing proprietary brands include VIBES Rolling Papers, Pollen Gear, the Marley Natural accessory line, Aerospaced & Groove grinders, Marley Natural, K. Haring Glass Collections, and Higher Standards. Effective March 2021, we added the Eyce product line to our proprietary brands.

In addition to absorbing the Marley Natural accessory line as a house brand, we are making other strides to ensure we take full advantage of the opportunities given to us as a company. We intend to extend the price points of the Higher Standards line to include a wider customer base, and in doing so, increase the presence of our house brands. To synergize with the direction of Higher Standards, and the K. Haring Glass Collection, both brands will sit under the Higher Standards brand umbrella. Taking this step is expected to ensure the brands are not competing against each other, and that we maximize market penetration for all our brands. With all these changes comes expansion into new markets; we are taking steps to ensure that all our proprietary brands are prepared to enter new markets in Europe during the upcoming year. In creating, acquiring, and expanding our proprietary brands, we intend to stay mindful of our key supplier relationships and to identify opportunities within our product portfolio and in the market where we can introduce or acquire compelling products that do not directly compete with the products of our core suppliers.

Execute on Identified Operational Initiatives.

We continue to evaluate operational initiatives to improve our profitability, enhance our supply chain efficiency, strengthen our pricing and category management capabilities, streamline and refine our marketing process and invest in more sophisticated information technology systems and data analytics. In addition, we continue to further automate our distribution facilities and improve our logistical capabilities. We are also taking steps to transition to a more centralized model with fewer, larger, highly automated facilities. During 2020, we made significant progress towards this goal through consolidating our distribution facilities in the United States into one primary streamlined centrally-located facility and one facility in California, primarily serving our S&P customers, which will reduce costs going forward. We believe we will continue to benefit from these and other operational improvements.

Be the Employer of Choice.

We believe our employees are the key drivers of our success, and we aim to recruit, train, promote and retain the most talented and success-driven personnel in the industry. Our size and scale enable us to offer structured training and career path opportunities for our employees, while in our sales and marketing teams, we have built a vibrant and entrepreneurial culture that rewards performance. We are committed to being the employer of choice in our industry.

Business Seasonality

While our B2B and B2C customers typically operate in highly-seasonal businesses, our Channel & Dropship and S&P divisions are less affected by the holidays. We have historically experienced only moderate seasonality in our business, particularly during the fourth quarter, which coincides with Cyber Monday (the first Monday after Thanksgiving, when online retailers typically offer holiday discounts), and as our customers build up their inventories in anticipation of the holiday season and for which we have related promotional marketing campaigns. Additionally, plans for growth in E-Commerce and more regularity in the B2B division will likely result in more consistent trends around the winter months, and the industry related holidays. For the year ended December 31 2020, seasonality was largely impacted by the COVID-19 pandemic. While we typically experience a substantial increase in sales for the "4/20" industry holiday, we saw a very minimal increase as our retail [brick and mortar] operations were closed and many of our B2B customers were closed for business as well. We also noticed increased revenue in the third quarter of 2020, as compared to the second quarter of 2020, which was largely driven by the lifting of quarantine restrictions and reopening of many businesses that previously were closed temporarily due to the pandemic. If these trends continue, we expect B2B and B2C retail sales to return to and exceed pre-COVID-19 revenue figures as the COVID-19 vaccines become more readily available.

Human Capital Resources

As of December 31, 2020, we had 264 full-time employees. Approximately 189 were employed in the U.S. and 75 were employed in Europe. None of our employees are represented by a labor union. We have never experienced a labor-related work stoppage.

As we mention in our core operating strategies, we aim to be the employer of choice, as our employees are the key drivers of our success. We aim to recruit, train, promote and retain the most talented and success-driven personnel in the industry. Our industry knowledge and scale provide opportunities for our employees to obtain structured training and career path opportunities across all departments and positions. We are a company built and based on trust, sincerity, respect, commitment, and fairness, and we strive to create a work environment that is friendly, open, and co-operative.

Employee Health and Safety during COVID-19

The health and safety of our employees is a top priority for us. During COVID-19, we were deemed an essential industry and as a result, we were very active in monitoring and tracking all relevant data, including guidance from local, national, and international health agencies. Our actions included:

•Allowing employees to work remotely where feasible;

•Implemented enhanced safety measures including mandatory face coverings, physical distance requirements, temperature checks, deep cleaning and disinfectant protocols, and hand sanitizing stations for employees continuing critical on-site work at all locations;

•Provide employee-wide training on COVID-19 safety measures;

•Restrict company travel to essential business travel that requires prior multi-level approvals.

Our Human Resources department is continuing to communicate to our employees as more information is available and continues to evaluate our operations considering federal, state, and local guidance.

Diversity and Inclusion

We are committed to diversity and inclusion across all aspects of our company. We have developed a diversity and inclusion committee (led by our employees) that is centered on educating our employees on the benefits of a diverse workforce, reducing the risk of bias and ensuring that everyone owns responsibility for inclusive behaviors and actions across the organization. We have established hiring principles that focus on our mission to hire people from diverse backgrounds who will add to our culture.

Culture and Engagement

Everything we do is powered by our vision and core values and our culture reflects that. As a result, we enjoy a highly motivated and skilled work force committed to our company. In 2020, we held our first employee engagement survey, and in consultation with our employees we have addressed several opportunities to further improve our culture. By being open, honest, and transparent, our employees feel more actively engaged in our success.

Total Rewards and Pay Equity

We strive to attract and retain diverse, high caliber employees who raise the talent bar by offering competitive compensation and benefit packages, regardless of their gender, race, or other personal characteristics. We regularly review and survey our compensation and benefit programs against the market to ensure we remain competitive in our hiring practices. We provide employee salaries that are competitive and consider factors such as an employee’s role and experience, the location of their job and their performance. In addition to our competitive salaries, to enhance our employees’ sense of participation in the company and to further align their interests with those of our stockholders, we offer equity packages to a broad set of key employees.

Development and Retention

We strive to hire, develop, and retain talent that continuously raises the performance bar. We encourage, support, and compensate our employees based on our philosophy of recognizing and rewarding exceptional performance. We believe that performance and development is an ongoing process in which all employees should be active participants. In 2020, we rolled out key performance goals for all employees linked to their compensation and have begun work on a Greenlane Learning and Development curriculum that will include a blended approach to both in person and virtual learning.

Competition

Business-to-Business. We operate in an evolving industry in which the market and its participants remain highly fragmented. Although it is difficult to find reliable independent research, we believe there is a vast number of potential B2B customers in North America comprised of independent retail shops, specialty retailers, licensed cannabis dispensaries and regional retailer chains.. We currently serve over 8,000 of these locations. Our B2B customers compete primarily on the basis of the breadth, style, quality, pricing and availability of merchandise, the level of customer service, brand recognition and loyalty. We successfully reach our B2B customers through our direct sales force and other marketing initiatives, and provide them with our strategically-curated mix of brands and products, merchandise planning strategies and exceptional customer service. Among vaporizer product distributors, we compete against both suppliers and other distributors. A number of suppliers choose to distribute directly in some sales channels and may also operate their own e-commerce platforms. We face competition from many small privately-owned regional distributors that carry a narrow range of products. We believe there are only a select few wholesale distributors carrying a complete line of premium vaporization products and consumption accessories.

Business-to-Consumer. A number of suppliers of vaporizers and specialized consumption products and accessories operate their own e-commerce websites through which they sell their items directly to end consumers. Additionally, there are hundreds of websites that sell products similar to those we offer in North America, Europe, Australia and other parts of the world. We believe we compete effectively with other e-commerce websites. Further, we provide fulfillment services to the owners of some of these websites as they do not carry their own inventory, are not able to ship as efficiently as we do and are unable to meet certain regulatory requirements, such as sales tax collection. Our competitors’ websites rank in many search categories below our primary e-commerce website, Vapor.com, which has its own dedicated design, social media and search engine optimization ("SEO") teams. We believe our market knowledge, large product selection, relationships with vaporizer brands, in-house search engine optimization teams, social media focus and distribution facilities will enable us to remain a market leader in e-commerce.

Trademarks

We own a number of registered trademarks and service marks, including without limitation, Greenlane, Higher Standards, VIBES, Aerospaced, Groove, Pollen GearTM, and most recently Eyce. Solely for convenience, trademarks and trade names referred to in this Form 10-K may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. In addition, this Form 10-K contains trade names, trademarks and service marks of other companies that we do not own. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, these other companies. We believe our largest trademarks are widely recognized throughout the world and have considerable value. The duration of trademark registrations varies from country to country. However, trademarks are generally valid and may be renewed indefinitely as long as they are in use and/or their registrations are properly maintained.

Insurance

We carry a broad range of insurance coverages, including general liability, real and personal property, workers’ compensation, directors’ and officers’ liability and other coverages we believe are customary. Our exposure to loss for insurance claims is generally limited to the per-incident deductible under the related insurance policy. We do not expect the impact of any known casualty, property, environmental or other contingency to have a material impact on our financial conditions, results of operations or cash flows.

Our directors’ and officers’ liability insurance policy we chose to maintain covers only non-indemnifiable individual executive liability, often referred to as “Side A,” and does not provide individual or corporate reimbursement coverage, often referred to as “Side B” and “Side C,” respectively. The Side A policy covers directors and officers directly for loss, including defense costs, when corporate indemnification is unavailable. Side A-only coverage cannot be exhausted by payments to the Company, as the Company is not insured for any money it advances for defense costs or pays as indemnity to the insured directors and officers. As a result, we currently do not have insurance coverage for, and directly self-funded with cash on hand, our litigation defense costs for actions like those described under "Item 3—Legal Proceedings".

Regulatory Developments

Our operating results and prospects will be impacted, directly and indirectly, by regulatory developments at the local, state, and federal levels. Certain changes in local, state, national, and international laws and regulations, such as increased legalization of cannabis, create significant opportunities for our business. However, other changes to laws and regulations result in restrictions on which products we are permitted to sell and the manner in which we market our products, increased taxation of our products, and negative changes to the public perceptions of our products, among other effects.

We believe the continuing trend of states’ legalization of medicinal and adult-use cannabis is likely to contribute to an increase in the demand for many of our products. In the 2020 election, voters approved ballot initiatives legalizing adult-use cannabis in New Jersey, Arizona, Montana and South Dakota. Voters also approved initiatives legalizing medical marijuana in Mississippi and South Dakota. Other states appear likely to legalize either medical or adult-use cannabis in 2021 and beyond. However, we can provide no assurances that additional states will legalize cannabis.

Recently, the identification of many cases of e-cigarette or vaping product use associated lung injury (“EVALI”) has led to significant scrutiny of e-cigarette and other vaporization products. Additionally, certain academic studies and news reports have suggested that smoking or vaping may increase the risk of complications for individuals who contract COVID-19. EVALI, COVID-19 and other public health concerns could contribute to negative perceptions of vaping and smoking, which in turn could lead consumers to avoid certain of our products, which would materially and adversely affect our results of operations.